BALTIMORE — Auto insurance is getting more expensive nationwide, including in Maryland. Just ask David Willeford. He was recently notified that his premium would increase over 33 percent.

Willeford is a senior on a fixed income with no tickets or accidents, but there are factors outside of his control causing rates to soar.

“I was in a state of shock when I opened it up,” said Willeford after receiving a notice from AARP Auto Insurance Program From The Hartford. “My total costs last year, this is just for two cars was $2,770. And this year, the total premium was $3,705.”

Willeford immediately called his insurance company for an explanation.

“She says, ‘Well, sure, you know, all insurance companies are going up, they're all raising their rates.’ She says the cost of doing business is increasing, the cost of parts and supplies and automobiles, and so forth, it just keeps going up,” Willeford said.

But he wanted to know why those costs are being passed along to him.

“How long have you been a customer of theirs?” WMAR-2 News Mallory Sofastaii asked Willeford.

“Fourteen years,” he responded.

“Have you had any recent accidents” Sofastaii asked.

“Never,” said Willeford.

“Do you have a new car?” asked Sofastaii.

“Nineteen, 2019. And a 2021,” he said.

“So did they give any other kind of explanation pertaining to your driving record or your choice in vehicle?” Sofastaii followed up.

“No, they commended me. They commended me,” Willeford said.

According to data from the consumer price index released in April, car insurance prices rose by an unadjusted 2.7 percent, while the year-over-year increased by 22.2 percent.

“I'm a consumer of auto insurance too, so I've had the same experience,” said Maryland Insurance Commissioner Kathleen Birrane, who heads the state agency that oversees and regulates insurers in the state.

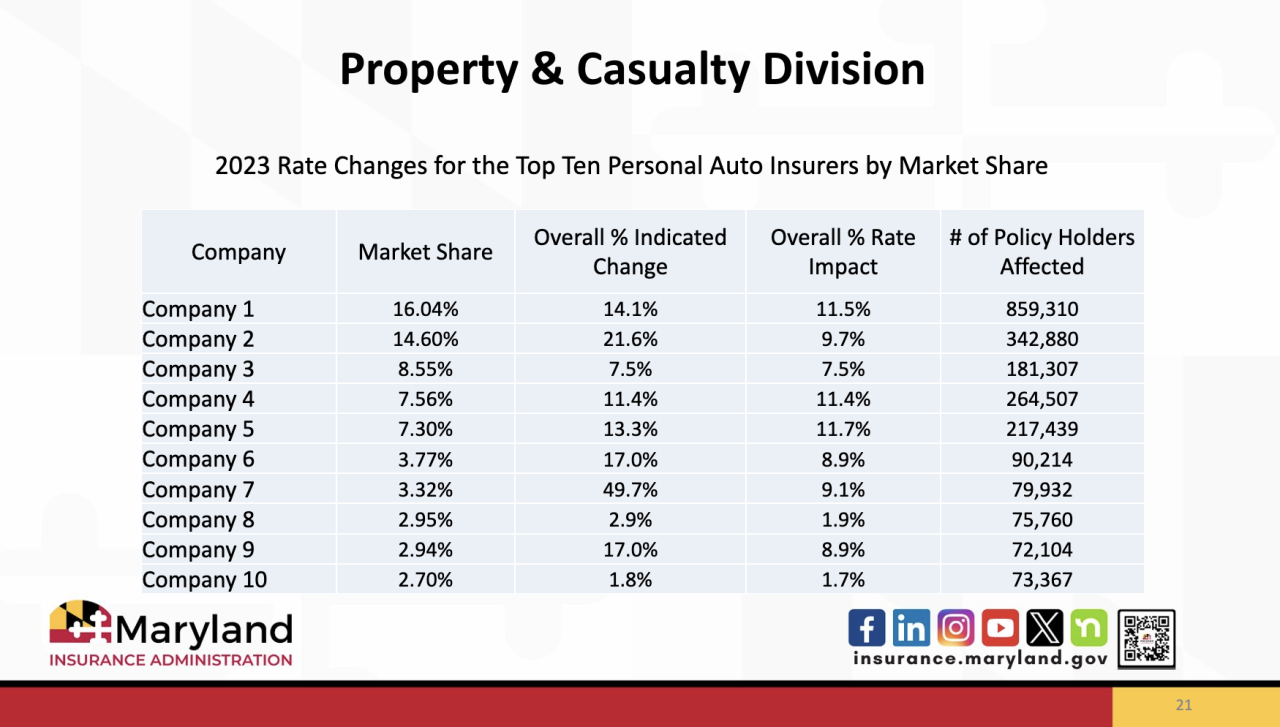

In a presentation to the Maryland General Assembly House Economics Matters Committee, the MIA gathered information from the top ten personal auto insurers by market share in Maryland. In 2023, rates increased for all 10 companies, but varied between 1.8 percent and up to 49.7 percent. The MIA said they're unable to provide the names of these companies.

“The primary driver of the increase in premium is the increase in losses that insurance companies are required to pay — the cost of an accident, the cost of parts, the cost of medical care when there's a bodily injury claim, the cost of a jury verdict and the amounts of verdicts that are increasing over time,” Birrane explained.

Carriers must have enough capital to remain solvent, so more losses means more money is needed to be able to cover future claims.

"File and Use" vs. "Prior Approval"

Maryland is also what's called a “file and use” state meaning insurers file rates and may use the rates without the MIA’s prior approval.

“Our job is to review them and to make sure that they meet certain standards, that is they're not unfairly discriminatory, that they are actuarially sound, that they are not excessive,” said Birrane.

Sofastaii asked for her definition of an excessive increase.

“Only if there isn't enough competition in this space could I conclude that a rate is excessive, and there is a lot of competition in this space,” Birrane responded.

However, in 12 states and most recently Washington D.C., insurance regulators do have that power and require prior approval before insurers can change their rates.

Birrane added that Maryland has considered becoming a prior approval state, but she doesn't believe it would make much of a difference.

“Prior approval does not equal changing the cost drivers. So, prior approval means I have more wiggle room to be able to say, I think that's excessive, and you know, you ought t to drop this piece down or that piece down in some way, but if you look at D.C. as an example, so far, I don't think we've seen a whole lot of difference between what the rates are between prior approval and competitive,” said Birrane.

Shop for a competitive rate

Her solution for policy holders is to aggressively shop around. The MIA has an online tool where you can compare insurance rates. You can also ask for discounts for driver history and partner programs.

Willeford was offered a $300 if he raises his deductible from $500 to $1,000, but that increases his out-of-pocket costs should he need to file a claim. “It does affect my budget, and my wife and I are retired. We're 77 years old, we drive very little, but still, you know, we're on a fixed income,” said Willeford.

Willeford added that his homeowner's insurance premium also increased by $350 a year. He's now looking around before switching companies.

Policy holders who see rate increases of more than 15 percent can file a complaint with the MIA. Birrane said, oftentimes, the adjustments are accurate but they can help you better understand what contributed to the increase and where to shop to find a better rate.

For additional information on how to lower your insurance rates, the MIA has provided a tip sheet for drivers on common discounts.

Commissioner Birrane also recommends working with an independent insurance agent who has the ability to write for multiple companies. And to make sure your information is up to date with your carrier. Certain factors like how many people are on your plan and how many miles you drive could impact how much you pay.

WMAR-2 News reached out to The Hartford for a response to Willeford’s rate increase. A spokeswoman declined to comment and referred WMAR-2 News to the American Property Casualty Insurance Association (APCIA).

In an email, Bob Passmore, department vice president of personal lines at the APCIA, wrote:

“Even if a driver has not had a claim or a ticket, auto insurance premiums have been on the rise for the simple reason that the cost of what goes into auto insurance has been rising. In 2022, auto insurance claims and expenses spiked to more than $1.12 for every $1 in premium.

Cumulative years of record-high inflation have greatly increased the cost of repairing and replacing cars. The increasing sophistication of the technology in today’s vehicles is also contributing to rising costs. Vehicles with advanced technology, like cameras and sensors, require more parts to be replaced, higher labor costs, and additional operations for scanning and calibration of systems. This means that repair costs have risen to their largest year-over-year increase. These more complex and expensive repairs are also taking longer, and that shows up as higher rental vehicle costs.

Recent reports have also shown that Americans are engaging in riskier driving behavior, such as speeding, distracted driving, and impaired driving, which increases injury and collision claims costs and compounds the effects of inflation. Insurers are urging drivers to reduce their risk by avoiding driving behaviors like distracted driving, speeding, and impaired driving that may result in a crash.

Any strain on insurance affordability and availability is a serious concern. The property casualty insurance industry is analyzing these issues and advocating for solutions to address increasing insurance costs for families, individuals, and business owners. Insurers are advocating for better infrastructure, including reliable supply chains for critical auto parts and safer roads, which should result in fewer crashes, and controlling claims costs to help keep insurance premiums affordable for consumers.”